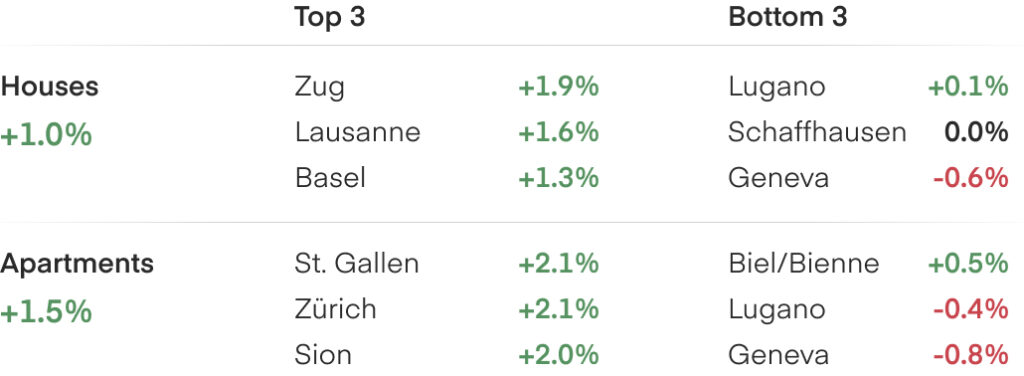

Quarterly change in real estate prices as of 31 December 2025

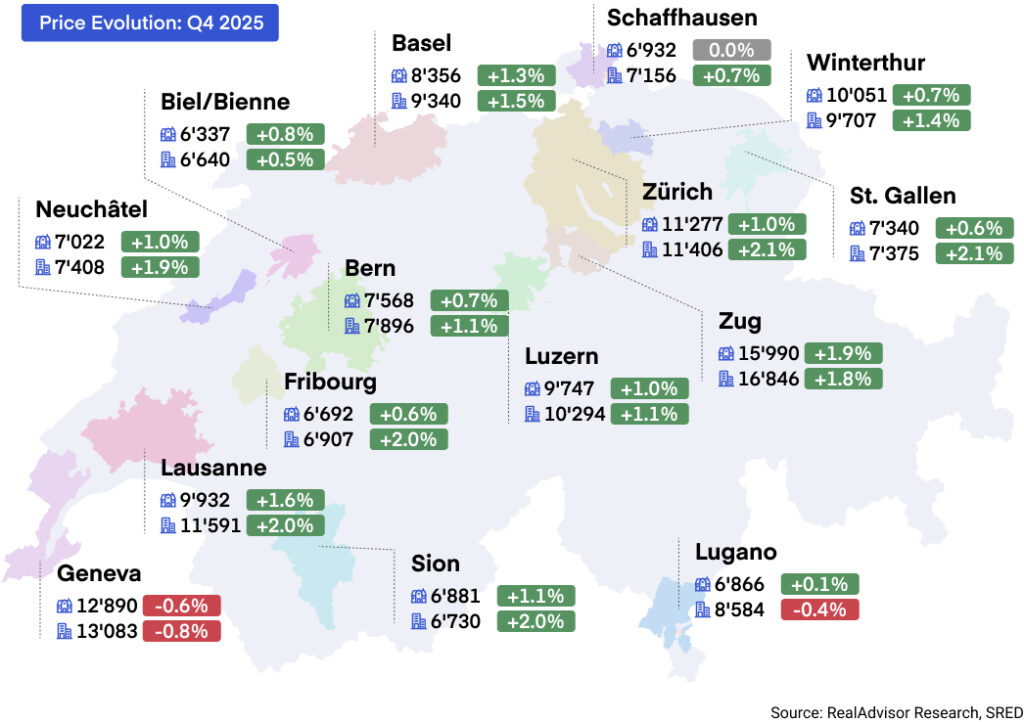

Average price per m² of houses and apartments

Q4 2025: Price changes in the 15 largest urban areas

Transactions Rebound as Prices Continue to Rise

The Swiss real estate market completed its recovery in 2025, with prices, transactions, and construction activity all turning decisively positive for the first time since 2021. Apartment prices rose 3.1% and house prices 2.4%, marking the second consecutive year of acceleration. Transaction volumes increased approximately 7%, the first positive year since 2021, though activity remains well below historic levels. For 2026, we expect moderate price growth of 2–3%, underpinned by tight supply and favourable financing conditions.

Price Growth Accelerates for the Second Successive Year

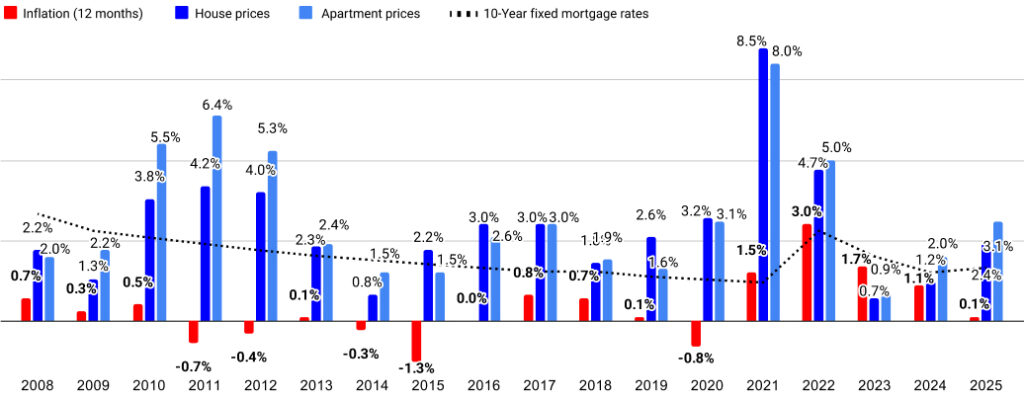

In 2025, Swiss property prices continued to accelerate, building on the momentum established in 2024. Apartment prices rose by 3.1%, up from 2.0% in 2024 and 0.9% in 2023. Single-family houses increased by 2.4%, double the 1.2% recorded a year earlier and well above the 0.7% seen in 2023. This marks the fourth consecutive year in which apartments have outperformed houses, though the gap has narrowed sharply, from 0.8 percentage points in 2024 to 0.7 percentage points in 2025. House prices, which had lagged significantly since 2022, have now largely caught up. With inflation at 0% for the year, all gains represent real price growth. This stands in notable contrast to 2023, when inflation eroded much of the nominal increase.

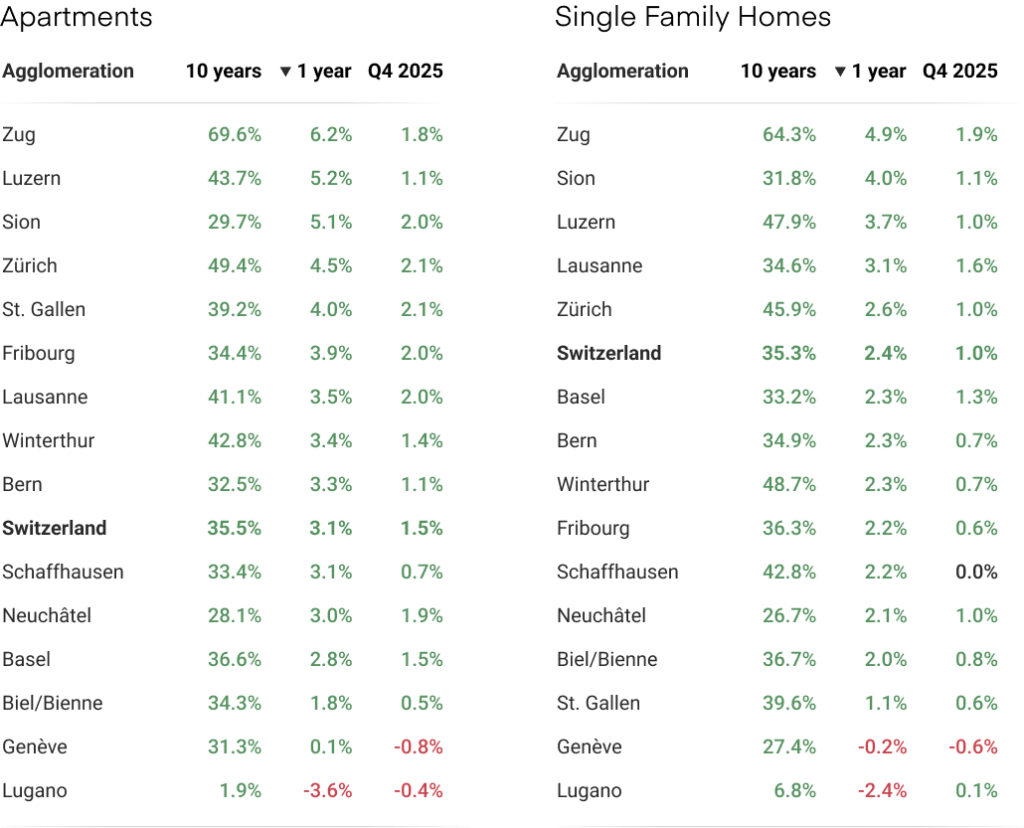

Across the 15 largest agglomerations, 14 out of 15 recorded price growth for apartments over the year. Zug (6.2%) and Luzern (5.2%) led the market, followed by Sion (5.1%), Zürich (4.5%), and St. Gallen (4.0%). These gains reflect continued strong demand in Central Switzerland and selected Romandie markets. Lugano was the only agglomeration to post a decline, with apartment prices falling 3.6% and house prices down 2.4%, extending a multi-year pattern of weakness in Ticino. Geneva showed a notable divergence between segments: apartments were essentially flat (0.1%) while houses edged down (−0.2%). This split may suggest an affordability ceiling, where buyers face tighter financing constraints.

At the cantonal level, Schwyz delivered the strongest performance of the year. Apartment prices rose 8.2%, well ahead of any other canton and more than double the national average. It was followed by Zug (6.4%), Graubünden (5.8%), Appenzell Innerrhoden (5.7%), and Fribourg (5.2%). The dominance of Central Switzerland is now unmistakable: Schwyz, Zug, Luzern, Nidwalden, and Obwalden all ranked among the top ten cantons for apartment price growth. Graubünden's strong result (5.8%) likely reflects sustained demand for Alpine and second-home properties. At the other end of the spectrum, Ticino was the only canton to record negative growth, with apartments down 2.6% and houses down 1.9%. This marks its fourth consecutive year of underperformance, pointing to deeper underlying challenges in the region. Jura (0.1%) and Uri (0.5%) also lagged, though both remained in positive territory.

Overall, 2025 confirmed the market's return to sustained and broad-based growth. Price increases were recorded in 25 of 26 cantons and 14 of 15 major agglomerations for apartments. Regional divergence continues to widen: Central Switzerland is pulling further ahead, while Ticino remains persistently weak. The market shows no signs of overheating or impending correction. It appears balanced, supported by resilient demand and constrained supply, with growth distributed across both urban centres and mid-sized regions.

How much is my home worth?

Enter your address to get an instant valuation with RealAdvisor.

Transaction Volumes Rise, Ending Three Years of Decline

After three consecutive years of decline, transaction volumes turned positive in 2025. The number of property sales increased by approximately 7% compared to 2024, which had marked the lowest level in over a decade. While this represents a welcome stabilisation, activity remains historically subdued, still roughly a third below the 2021 peak and well below the 10-year average. Market liquidity has improved, but a full recovery to pre-2022 levels has yet to materialise.

The improvement was driven primarily by stable, low interest rates. The SNB cut its policy rate six times between early 2024 and mid-2025, bringing it from 1.75% to 0%. Over the same period, 10-year mortgage rates settled around 1.6–1.7%. These conditions allowed buyer and seller expectations to converge after years of standoff, gradually releasing some of the pent-up demand that had accumulated since 2022. The recovery was broad-based, though not universal: Geneva recorded 3,619 transactions, down from 3,754 in 2024, a reminder that supply constraints continue to limit activity in the country's tightest markets.

Inventory dynamics varied sharply by region, and these differences correlate closely with price performance. Nationally, the number of properties on the market fell to approximately 43,700 at year-end, down from 45,000 a year earlier. But the picture differs dramatically across cantons.

In Central Switzerland and Zurich, supply tightened further: listings fell 19.4% in Zug, 11.7% in Zurich, and 5.5% in Luzern. These are also the cantons with the strongest price growth and the fastest-moving markets, with median time on market as low as 68 days in Zug and 74 days in Schwyz and Luzern. At the other end of the spectrum, Ticino saw listings rise 19.5%, bringing its total to over 10,000 properties, by far the highest in the country. Properties there take a median of 192 days to sell, nearly three times longer than in Zug. Jura recorded an even sharper increase in listings (46.2%) and a median time on market of 125 days. The pattern is consistent: where supply is tight and turnover is fast, prices are rising; where inventory is accumulating and properties sit longer, the market is struggling.

Construction activity showed signs of recovery, with the residential construction index returning to 100 points (its Q1 2023 baseline) in the fourth quarter for the first time in two years, signalling that activity has recovered to pre-downturn levels. Yet demand continues to outpace supply across most of Switzerland. With the population exceeding 9.1 million and Swiss owners holding properties for an average of 30 years, available inventory turns over slowly. Until new construction catches up, the structural imbalance will continue to support prices in the most constrained markets while leaving others, like Ticino and Jura, to work through their surplus.

Yearly transaction volume evolution, 2012 to today

Outlook — Moderate Price Growth to Continue in 2026

The Swiss real estate market delivered on the recovery signalled in our Q3 report. Price growth landed slightly below our forecast of 3.0–3.5%, with apartments up 3.1% and houses up 2.4%. Transaction volumes recovered more strongly than anticipated, rising 7% after three years of decline. The construction index returned to its baseline of 100 points for the first time in two years.

With the recovery now confirmed, the question turns to sustainability. In January, Swiss 2-year government bond yields returned to negative territory for the first time since 2022, while SARON—the benchmark for variable-rate mortgages—also dipped below zero. This is a significant signal: bond markets are now pricing in the possibility that the SNB may need to cut rates below zero if economic conditions deteriorate further. At the World Economic Forum in Davos, SNB Chairman Martin Schlegel acknowledged that Swiss inflation could turn negative in some months of 2026, reinforcing this view. While the SNB held its policy rate at 0% in December and is expected to maintain this level throughout 2026, the return to negative yields suggests the floor for financing costs may be lower than previously assumed.

For property buyers, this has clear implications: the ultra-low rate environment is not only here to stay—it could deepen. Mortgage rates for 10-year fixed loans have stabilised around 1.6–1.7%, while SARON-linked mortgages now carry effective rates below 1%. If the SNB were to move into negative territory, fixed-rate mortgages could fall further, though most lenders floor SARON mortgages at zero. Either way, the cost of owning property is unlikely to rise meaningfully in the near term, which should continue to support demand—particularly given that owning remains cheaper than renting in many parts of the country.

The broader economic outlook is more muted. GDP growth is expected to slow to around 1% in 2026, below the long-term average, and unemployment is likely to rise modestly. However, weak growth is precisely what is keeping rates so low. For the property market, this creates a supportive paradox: the same economic softness that might dampen confidence also ensures financing remains exceptionally cheap.

For 2026, we expect price growth to moderate to around 2–3%. The fundamental driver remains unchanged: demand continues to outpace supply, and inventory is tight. Regional divergence will persist. Central Switzerland, where supply is tightest and turnover fastest, is likely to continue outperforming. Ticino and Jura, which face a persistent supply overhang, may see further stagnation or declines. For most of the country, however, the outlook is one of continued, if moderate, growth.

Evolution of real estate prices in relation to inflation since 2008

Cantons: Evolution of single family home and apartment prices

Agglomerations: Evolution of single family home and apartment prices

Sources and Methodology

¹ RealAdvisor Research

² Cantonal statistical offices (Geneva, Zurich, Ticino) and Federal Statistical Office (FSO)

³ Swiss Real Estate Data Pool

⁴ Swiss Contractors’ Association (SSE)

⁵ Swiss National Bank (SNB)

⁶ Geneva Chamber of Notaries, RealAdvisor Finance

⁷ Federal Reserve / European Central Bank (ECB)

Additional information

- Property prices in Switzerland

- Online Property Valuation Online

- Download the complete version of the barometer

Press contact

- press@realadvisor.com

- +41 (0) 22 552 46 46

RealAdvisor SA

Rte de Saint-Julien 198,

CH-1228 Plan-les-Ouates

RealAdvisor AG

Heinrichstrasse 200

CH-8005 Zürich

Suisse

Suisse España

España France

France Italia

Italia Belgique / België

Belgique / België Česko

Česko Deutschland

Deutschland Nederland

Nederland Österreich

Österreich Polska

Polska Portugal

Portugal United Kingdom

United Kingdom