Quarterly change in real estate prices as of 31 March 2026

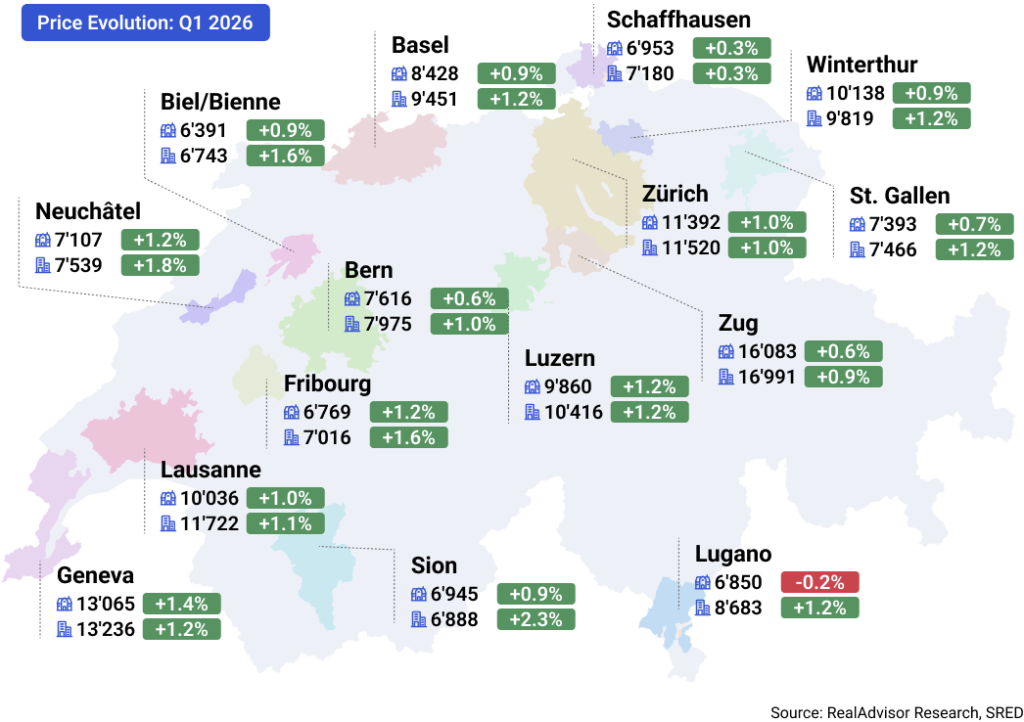

Average price per m² of houses and apartments

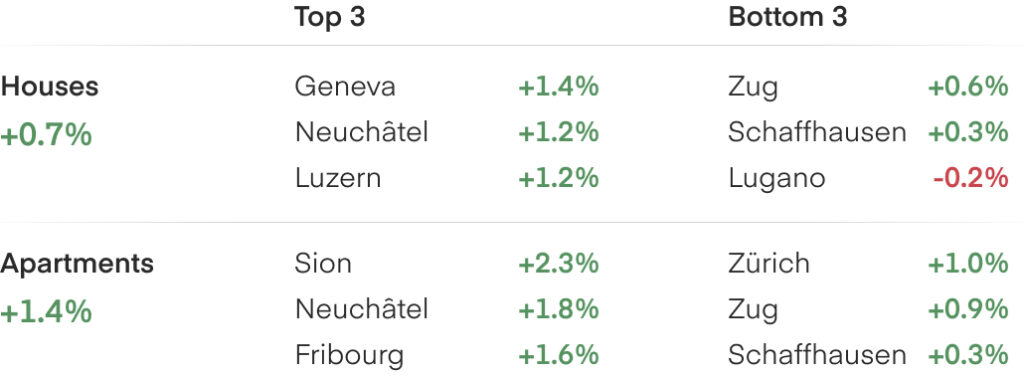

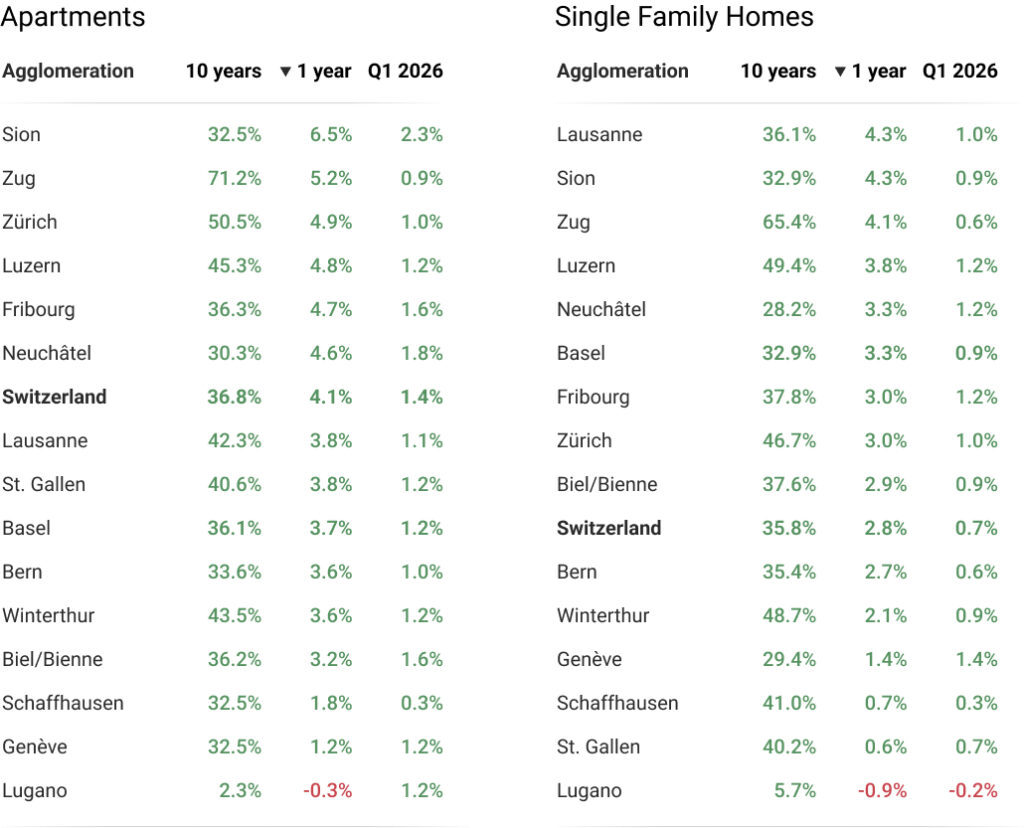

Q1 2026: Price changes in the 15 largest urban areas

Prices Rise Across Switzerland as Supply Stays Tight

Apartment prices rose across Switzerland in Q1 2026, gaining +1.4% over the quarter and +4.1% over twelve months while continuing to outperform single-family homes. The key tension is that supply is improving on paper but not yet on the ground: newly authorised dwellings rebounded to more than 52,000 in 2025, yet transaction activity is only recovering gradually and the lag from permits to completions keeps available housing tight. That mix supports a forecast near the upper end of our +2.5% to +3.0% range for 2026.

Price Growth Broadens Beyond the Strongest Markets

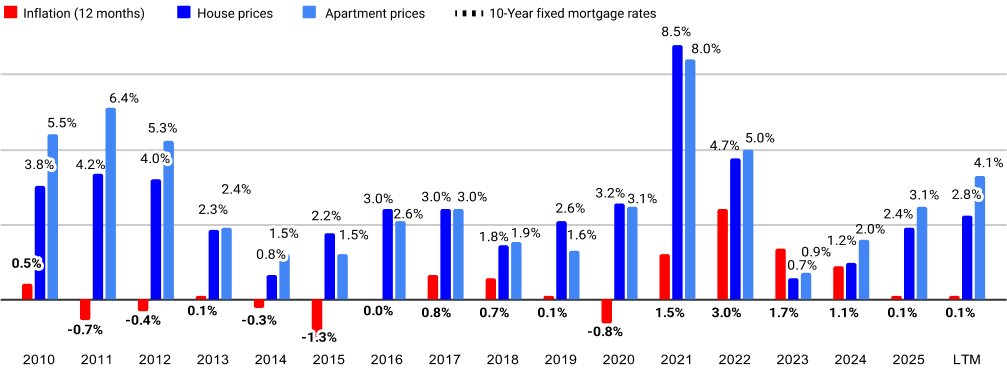

Swiss residential prices posted another positive quarter. At the national level, apartment prices rose by +1.4% quarter-over-quarter and +4.1% year-over-year. Single-family homes increased by +0.7% over the quarter and +2.8% over twelve months. With inflation at only +0.1%, these gains represent real price growth.

This extends a pattern visible in the past quarters: apartments have now grown faster than single-family homes in each of the last three quarters. The gap also widened this quarter, with apartments up +4.1% over twelve months compared with +2.8% for houses. The breadth of the move matters too: apartment prices rose in every main agglomeration and in every canton, while house growth was positive in most markets but still more uneven. The breadth is more important than the ranking: even the slower apartment markets remained positive, from Schaffhausen at +0.3% to Zürich at +1.0% and Lugano at +1.2%.

The strongest gains came from outside the usual core. For apartments, Sion led at +2.3%, followed by Neuchâtel (+1.8%) and Fribourg (+1.6%). For single-family homes, Genève led with +1.4%, with Neuchâtel and Luzern both at +1.2%. The result is a more Romandie- and Alpine-tilted quarter than late 2025, when Zürich and Zug dominated the table.

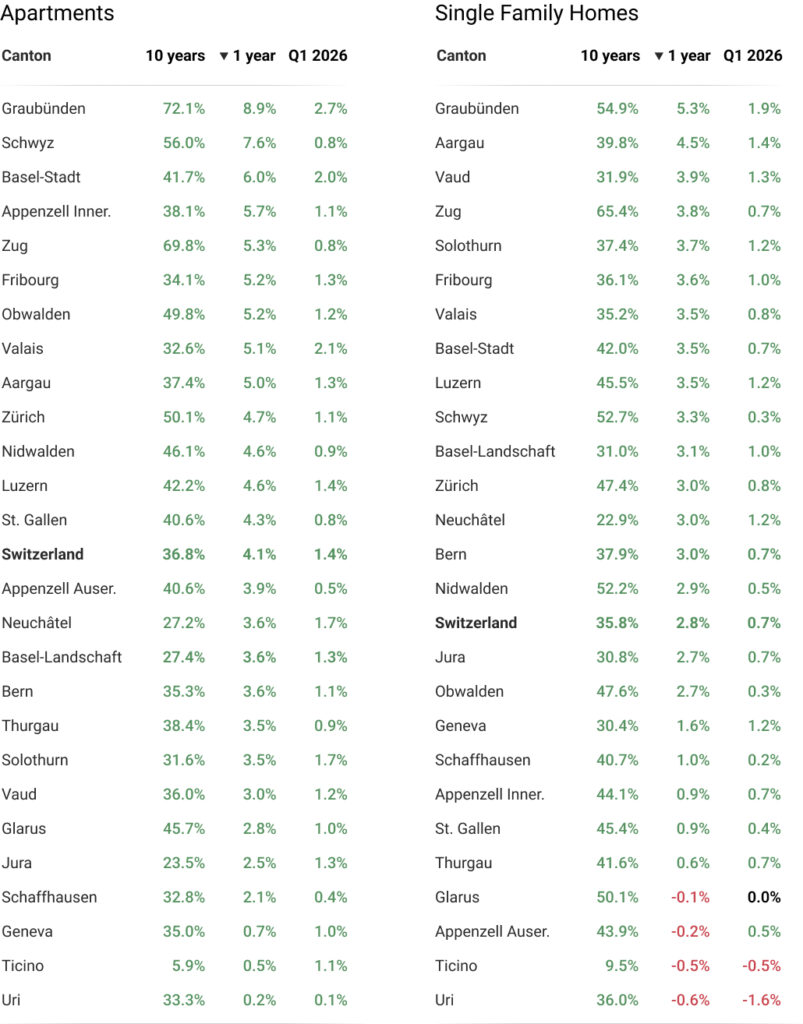

The canton data confirms the same pattern at a wider lens. Apartment growth was strongest in Graubünden (+2.7%), Valais (+2.1%) and Basel-Stadt (+2.0%), with houses led by Graubünden (+1.9%), Aargau (+1.4%) and Vaud (+1.3%). No single metropolitan market is driving the quarter.

The exception is Lugano, where house prices fell -0.2% over the quarter, consistent with Ticino's softer recent pattern. Compared with Q4 2025, Genève improved materially across both segments, Zug cooled from late-2025 outperformance, and Ticino has not yet shown a clean sign of reversal.

How much is my home worth?

Enter your address to get an instant valuation with RealAdvisor.

Market Remains Tight Despite a Rebound in 2025 Permit Approvals

Transaction activity is recovering, but the improvement is still gradual. Switzerland recorded an estimated +5% increase in transaction volumes in 2025, after +2% in 2024. That marks two consecutive positive readings, but it follows a deep correction: activity had fallen by -13% in 2022 and -20% in 2023. The latest twelve-month snapshot points in the same direction, with activity up by about +4.7% year-over-year.

That distinction matters. The market is not being pushed higher by a broad liquidity boom or a sudden return of speculative turnover. Prices are rising while transaction activity is still recovering from the last downturn, which reinforces the central reading of the quarter: scarcity, not excess liquidity, is setting the price.

The supply side is also moving in the right direction, but not fast enough to change the balance quickly. The residential construction index is up about +6% year-over-year and has now recovered roughly +8% from its late-2024 low, confirming that residential building has cleanly turned up from its 2024 trough. The Société Suisse des Entrepreneurs also identifies residential building as the main growth driver for 2026.

Permit data point in the same direction but also expose the main bottleneck for 2026. Newly authorised dwellings rebounded to more than 52,000 in 2025, up from roughly 41,000 in 2023. SECO notes that the gap between approval and actual construction usually runs for several quarters and can exceed a year for larger projects, so the rebound mainly supports activity over the coming quarters rather than today's tight market. The issue is not only whether projects are approved, but how quickly approvals can become completed homes.

On the demand side, the imbalance has not eased. Population growth in 2025 stayed solid in several already tight markets — Basel-Stadt (+1.37%), Valais (+1.26%), Genève (+1.08%), Aargau (+1.05%) and Vaud (+0.97%) — and international migration remained high relative to population in Basel-Stadt, Genève, Valais, Vaud and Zürich. Buyer search activity points the same way: Realmatch360 recorded a +4.3% increase in demand for owner-occupied apartments in 2025, while available for-sale listings shrank from roughly 42,000 to below 40,000 per quarter. SECO and the SNB both forecast Swiss GDP growth of around +1% in 2026, well below the historical average, so demand growth is moderating but remains firm enough to keep the market tight while supply catches up.

Yearly transaction volume evolution, 2012 to today

Outlook: Low Mortgage Rates Fuel Steady Growth, Anchoring the +3% Forecast for 2026

In the fourth quarter of 2025, RealAdvisor expected Swiss residential prices to rise by around +2.5% to +3.0% in 2026. The first three months of the year support the direction of that forecast, but the stronger apartment reading argues for the upper end of the range. While some market indicators are more bullish, the gradual transaction recovery and softer macro backdrop argue against a much more aggressive forecast.

Financing conditions remain highly supportive. The SNB policy rate stands at 0.0%, inflation is only +0.1%, and representative 10-year fixed mortgage rates are around 1.4%. The Swiss yield curve remains upward sloping, with short-term Confederation bond yields slightly negative and 10-year yields sitting near 0.4%. This structure keeps short-term SARON mortgages exceptionally cheap, while fixed-rate mortgages are more likely to remain broadly stable than to fall sharply from here.

The macro environment provides a balanced backdrop, but the potential impact of energy prices should be monitored. The SNB and SECO forecast 0.4% to 0.5% inflation, factoring in some impact from higher energy costs. March inflation rose to 0.3%, mainly because of heating oil, though this remains low by international standards. If oil prices normalise, the SNB can easily look through the shock and leave rates at zero. If the conflict lasts and energy costs spread into transport and wages, fixed mortgage rates could move modestly higher.

The growth picture points to a steady rather than booming market. SECO expects Swiss GDP growth of around 1.0% in 2026, below the long-term average, partly because higher energy prices and uncertainty weigh on consumption and investment. Employment growth and immigration are also expected to cool, which should limit additional demand pressure. In other words, the base case is supportive for property values because financing remains cheap, but it is not an acceleration environment.

There is one upside risk specific to the high-end segment. Renewed geopolitical uncertainty, particularly around the Middle East, is reinforcing Switzerland's traditional safe-haven appeal for wealthy households looking for stability and a European base. This could add support to prime markets such as Genève, Zug, Zürich, Vaud or Alpine resorts, especially at the luxury end. It should not drive the national forecast, but it highlights the resilience of the upper end of the market.

For 2026, we now expect Swiss residential prices to rise by around +3.0%, slightly above our Q4 2025 view. Apartments are likely to sit at the upper end of the +2.5% to +3.0% range, while houses should track closer to the middle. Low rates and tight supply continue to support prices, but weaker growth, cooling immigration, affordability constraints and only gradual transaction recovery argue against extrapolating the strongest signals from this quarter too far

Evolution of real estate prices in relation to inflation since 2010

Cantons: Evolution of single family home and apartment prices

Agglomerations: Evolution of single family home and apartment prices

Sources and Methodology

¹ RealAdvisor Research

² Cantonal statistical offices (Geneva, Zurich, Ticino) and Federal Statistical Office (FSO)

³ Swiss Real Estate Data Pool

⁴ Swiss Contractors’ Association (SSE)

⁵ Swiss National Bank (SNB)

⁶ Geneva Chamber of Notaries, RealAdvisor Finance

⁷ Federal Reserve / European Central Bank (ECB)

Additional information

- Property prices in Switzerland

- Online Property Valuation Online

- Download the complete version of the barometer

Press contact

- press@realadvisor.com

- +41 (0) 22 552 46 46

RealAdvisor SA

Rte de Saint-Julien 198,

CH-1228 Plan-les-Ouates

RealAdvisor AG

Heinrichstrasse 200

CH-8005 Zürich

Suisse

Suisse España

España France

France Italia

Italia Belgique / België

Belgique / België Česko

Česko Deutschland

Deutschland Nederland

Nederland Österreich

Österreich Polska

Polska Portugal

Portugal United Kingdom

United Kingdom