Quarterly change in real estate prices as of September 30, 2025

Average price per m² of houses and apartments

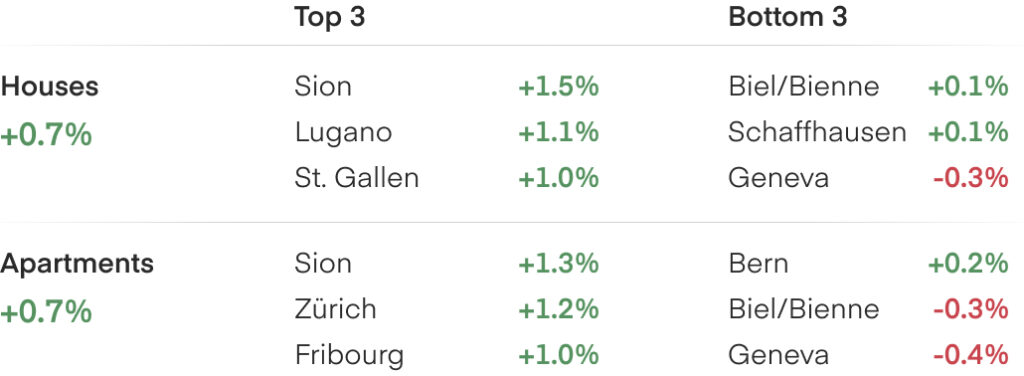

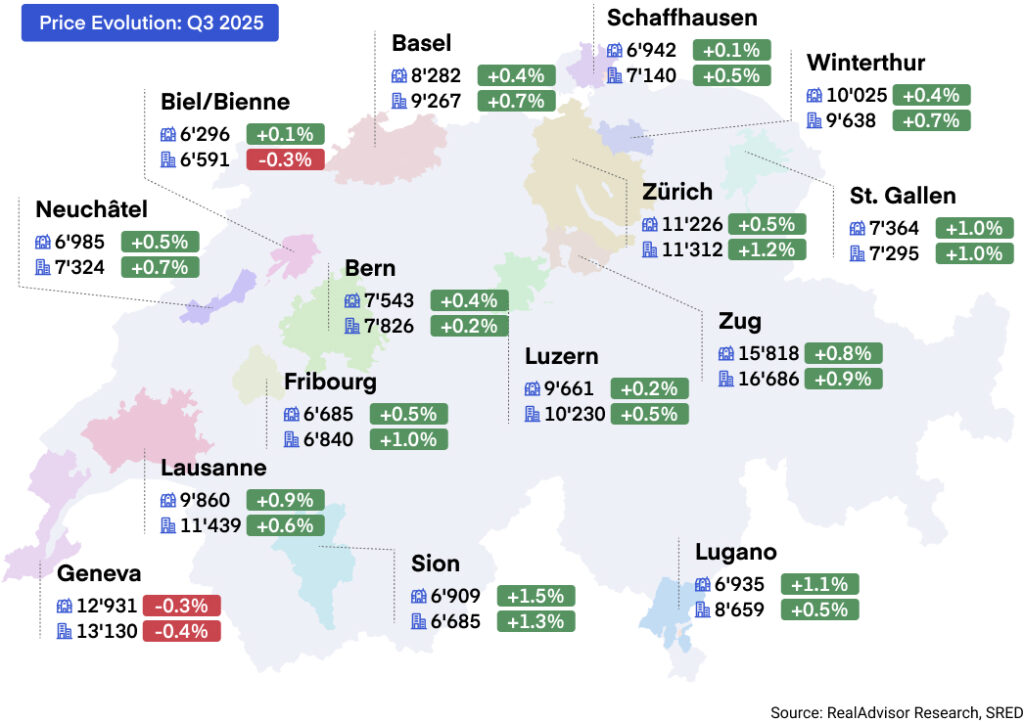

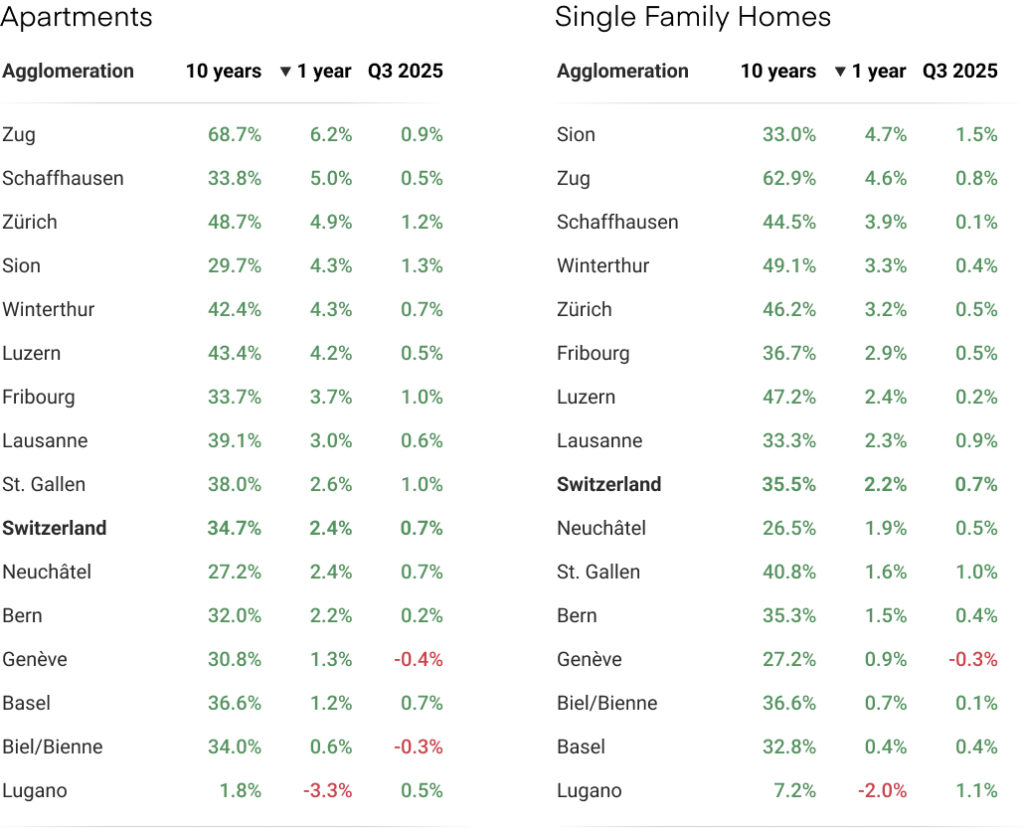

Q3 2025: Price changes in the 15 largest urban areas

Stable Price Growth with Eyes on New Tax Reform

The Swiss real estate market remained stable in the third quarter of 2025, with prices for both apartments and single-family houses rising by +0.7%¹. Transaction activity continued to strengthen, marking the highest annual growth rate in two years, while construction output showed only moderate progress. Financing conditions remain highly favourable, but the recently approved tax reform abolishing the imputed rental value may further tighten supply in the years ahead. Prices are now forecast to rise by around +3% to +3.5% for the full year.

Price Growth Remains Stable

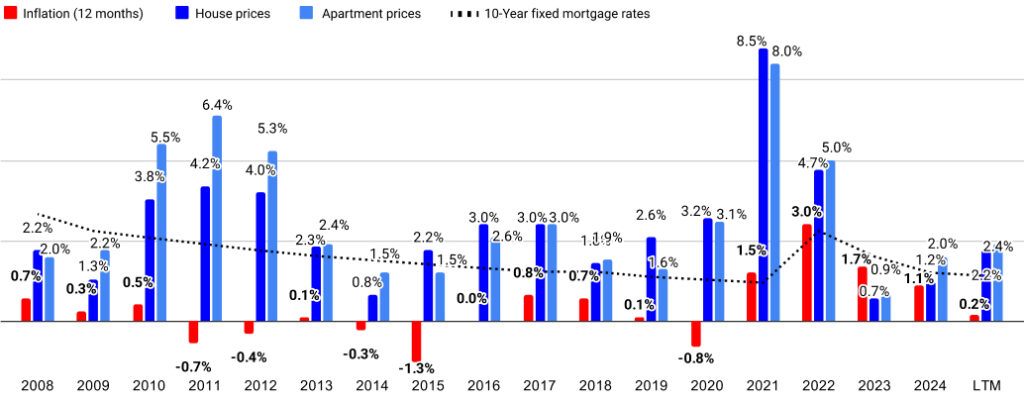

Property prices increased by +0.7%¹ for both apartments and single-family houses in the third quarter of 2025, reinforcing the picture of a balanced market that has gradually regained stability since 2023. Over the past twelve months, apartment prices have risen by +2.6%, the same rate as in the previous year, while house prices are up by +2.2%, compared with +1.2% a year earlier. This shows that apartment prices have maintained a steady pace of growth, whereas single-family homes have recovered part of the ground lost in earlier quarters, narrowing the gap between the two segments.

Across the main urban areas, price movements were moderate to strong, with most agglomerations recording quarterly increases. Apartment prices rose the most in Sion (+1.3%) and Zürich (+1.2%), followed by Fribourg and St Gallen (each +1.0%). Only Geneva (-0.4%) and Biel/Bienne (-0.3%) showed slight decreases. For single-family houses, the largest quarterly gains were seen in Sion (+1.5%), Lugano (+1.1%) and St Gallen (+1.0%), while Geneva (-0.3%) again edged lower. Overall, the data point to a quarter of broad-based growth across most major centres, with no signs of a general slowdown. Over the past twelve months, all major agglomerations have recorded positive growth, with Lugano standing out as the only area showing a marginal decline on an annual basis.

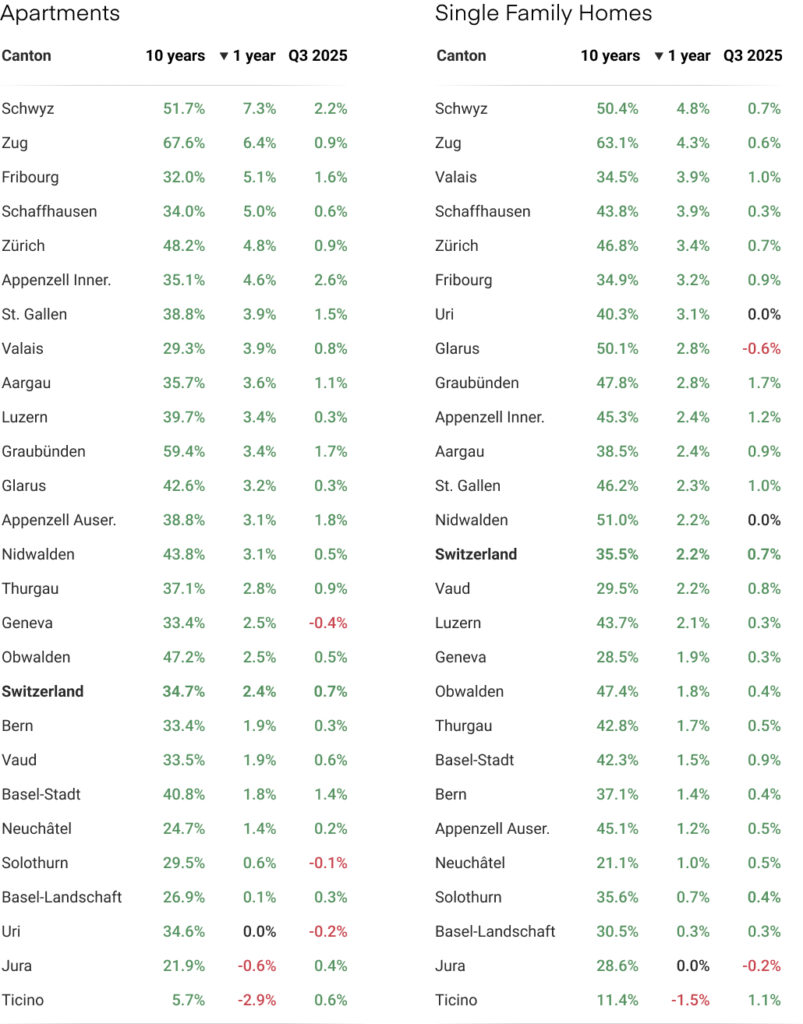

At the cantonal level, quarterly results showed consistent increases across most regions. Apartment prices rose most in Appenzell Innerrhoden (+2.6%), Schwyz (+2.2%) and Fribourg (+2.6%), while Genève (-0.4%) and Uri (-0.2%) registered small declines. For houses, Graubünden (+1.7%), Ticino (+1.1%) and Valais (+1.0%) led the gains, with only Glarus (-0.6%) and Jura (-0.2%) in negative territory. Some short-term variations diverged from the broader yearly pattern: despite a solid quarterly rebound, Ticino remained negative year-on-year, while Geneva, after a mild quarterly decline, still ranks among the cantons with above-average annual growth. These mixed signals underline that quarterly movements should be interpreted cautiously and assessed again at year-end to confirm whether they mark a lasting shift or short-term adjustment.

Overall, the third quarter confirmed the general stability of residential property prices in Switzerland. Differences between cantons and their main urban centres remain limited, as most continue to move in a similar direction. The market appears largely homogeneous at the national level, with only a few regional contrasts. Central Switzerland continues to outperform the rest of the country, while more peripheral areas such as Jura and Ticino still show weaker momentum. Urban centres remain solid overall, and no new patterns can yet be clearly identified.

Transaction and Construction Volumes Continue to Increase

Transaction activity strengthened further in the third quarter of 2025, extending the upward trend observed since the beginning of the year. The number of property sales increased by around +3% compared with the previous quarter and nearly +20% over the past twelve months—the highest annual growth rate in two years¹,³. This confirms that the market has entered a phase of sustained recovery after the sharp contraction seen in 2023. The renewed dynamism remains broad-based across property types, reflecting both improved buyer confidence and a continued normalisation of market conditions.

Regional patterns point to a rebalancing of activity between large cities, mid-sized agglomerations, and suburban areas. Major urban centres such as Zürich, Geneva, and Basel still account for about 30%³ of all transactions, though their share has edged slightly lower from a year earlier. Mid-sized hubs like Lausanne, Bern, Fribourg, and Lugano now represent roughly one-fifth of the national total—their highest proportion in a decade—while periurban municipalities have remained stable to slightly higher at around 21%. Rural peripheries, by contrast, saw a marginal decline in turnover.

The recovery in Romandie, particularly in Vaud and Fribourg, mainly reflects a rebound from a weak 2024, while the German-speaking core remains structurally strong. Ticino and Jura continue to lag behind, consistent with their limited price growth. Overall, these trends suggest that activity is broadening geographically, supported by demand for areas offering a balance between affordability and accessibility.

On the supply side, construction indicators point to moderate progress but persistent structural constraints. The residential construction index rose by +0.6%⁴ year-on-year in the third quarter, as slightly more dwellings were completed than initially projected—around 44,000 versus the 42,000 planned at the start of the year. However, building permit values have fallen by 8%⁴ over the past twelve months, signalling that the rebound in construction output may not last. Current order books are expected to sustain activity into early 2026, yet the overall pace of new housing supply remains insufficient to meet demand. This limited pipeline continues to underpin prices and reinforces the sense of a market returning to balance through stable but firm demand rather than rapid expansion.

Yearly transaction volume evolution, 2012 to today

Outlook – Tax Reform May Tighten Supply, Keeping Prices Firm Despite Low Rates

The previous outlook projected price growth of about +4% for 2025, supported by improving demand and easy financing. The third quarter confirms the market’s ongoing recovery but at a slower pace. Prices rose by +0.7%¹ over the quarter and around +2.5% year-on-year, indicating a stabilised market rather than renewed acceleration.

Financing remains a key pillar of this stability. The Swiss National Bank kept its policy rate at 0% in September, while inflation held at +0.2%⁵. Mortgage rates for ten-year fixed loans are around 1.3–2.0%⁶, levels seen lower only in 2020–21. Abroad, expectations of rate cuts by the US Federal Reserve and a pause by the European Central Bank could exert further downward pressure on long-term yields, leaving the SNB room to stay neutral or ease slightly, provided the franc remains stable⁷.

A major policy change followed the 28 September 2025 referendum abolishing the imputed rental value and allowing cantonal property taxes on second homes, effective in 2028. The reform benefits low-debt households but removes deductions for mortgage interest and maintenance, penalising many first-time buyers.

It also favours new construction—where financing needs and upkeep costs are lower—while reducing the appeal of older properties requiring refurbishment. Its full impact remains uncertain, as cantons are free to introduce new levies to offset lost revenue. For now, given tight housing stock and resilient demand, price effects should remain contained, though second-home and renovation-heavy segments may prove more sensitive.

As noted earlier, construction output has improved slightly but remains well below structural needs. Combined with fiscal changes that may discourage older owners from selling, this persistent shortage of available housing is likely to keep inventories tight and prices firm, even as financing remains accessible.

Based on current indicators, the Swiss housing market should record gains of around +3.0% to +3.5% for 2025. While low rates continue to support demand, the new tax framework and chronic undersupply are expected to tighten availability further, maintaining moderate upward pressure on prices into 2026.

Evolution of real estate prices in relation to inflation since 2008

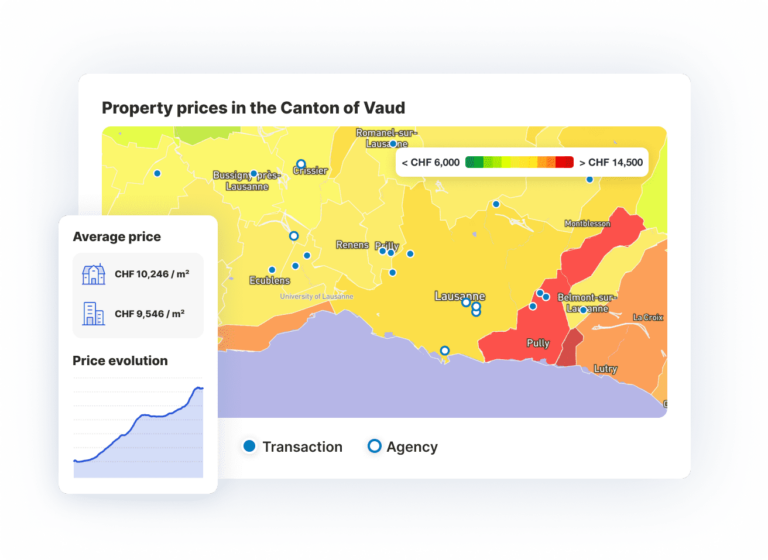

Cantons: Evolution of single family home and apartment prices

Agglomerations: Evolution of single family home and apartment prices

Sources and Methodology

¹ RealAdvisor Research

² Cantonal statistical offices (Geneva, Zurich, Ticino) and Federal Statistical Office (FSO)

³ Swiss Real Estate Data Pool

⁴ Swiss Contractors’ Association (SSE)

⁵ Swiss National Bank (SNB)

⁶ Geneva Chamber of Notaries, RealAdvisor Finance

⁷ Federal Reserve / European Central Bank (ECB)

Additional information

- Property prices in Switzerland

- Online Property Valuation Online

- Download the complete version of the barometer

Press contact

- press@realadvisor.com

- +41 (0) 22 552 46 46

RealAdvisor SA

Rte de Saint-Julien 198,

CH-1228 Plan-les-Ouates

RealAdvisor AG

Heinrichstrasse 200

CH-8005 Zürich

Suisse

Suisse España

España France

France Italia

Italia Belgique / België

Belgique / België Česko

Česko Deutschland

Deutschland Nederland

Nederland Österreich

Österreich Polska

Polska Portugal

Portugal United Kingdom

United Kingdom