Quarterly change in real estate prices as of 30th June 2025

Average price per m² of houses and apartments

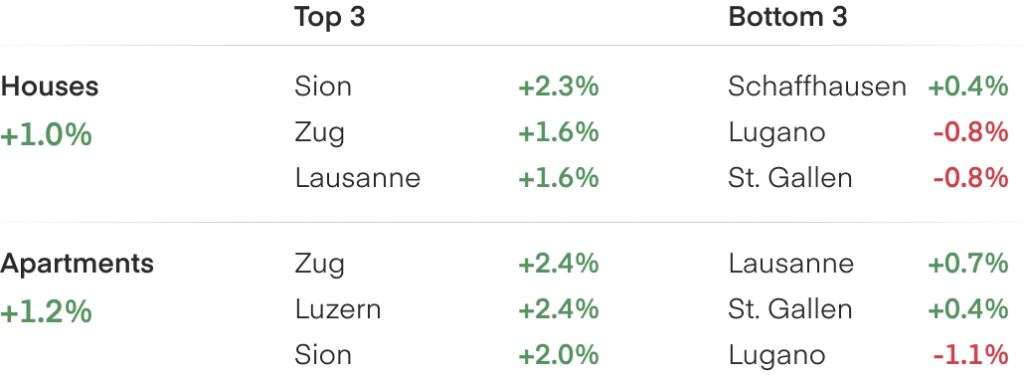

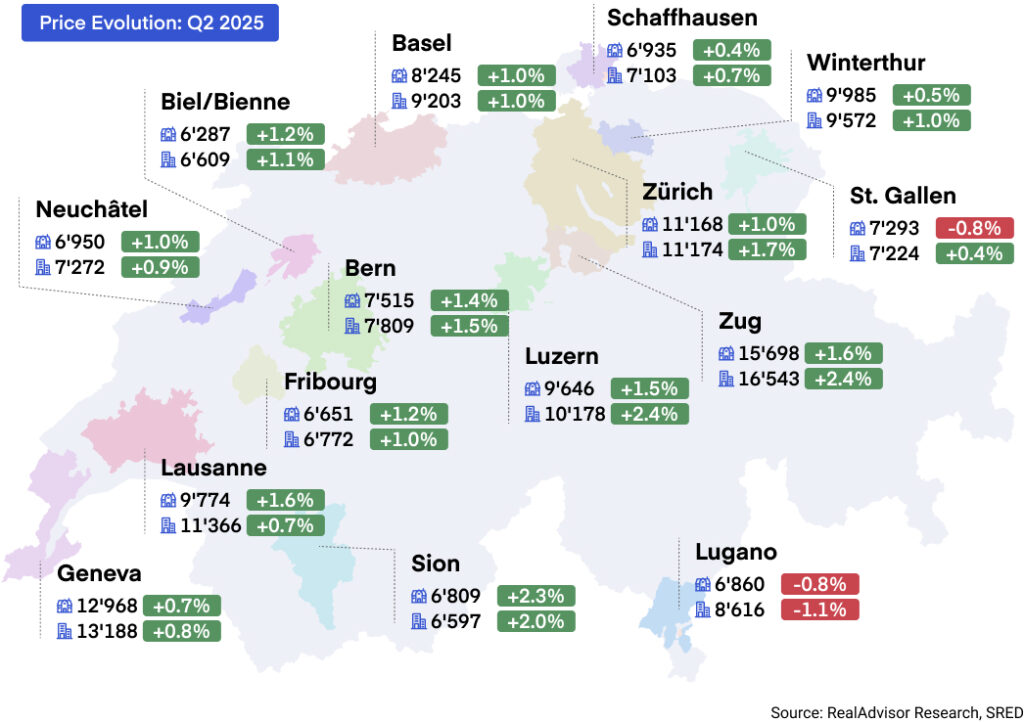

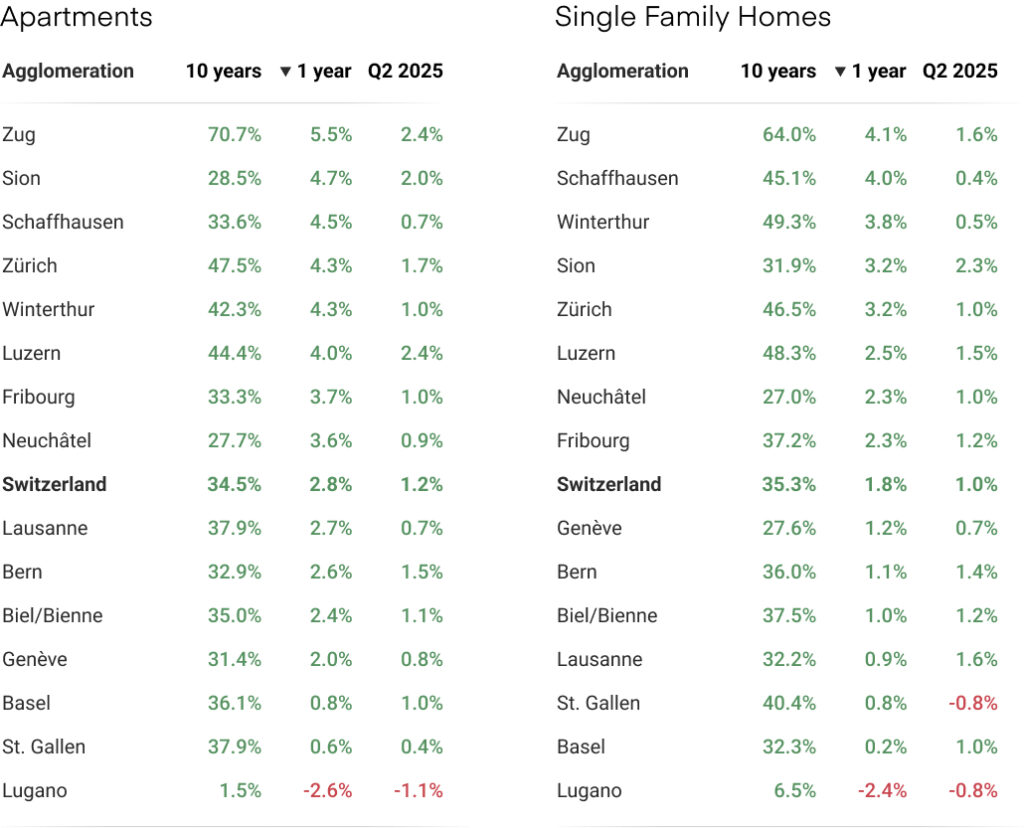

Q2 2025: Price changes in the 15 largest urban areas

Swiss Property Market Rebounds Sharply

The Swiss real estate market gained momentum in Q2 2025, with apartment prices rising by 1.2% and house prices by 1.0%, marking the strongest quarterly growth in three years. Transaction volumes continued to recover, supported by falling mortgage rates, stable inflation, and strong domestic demand. With supply remaining tight and financing conditions improving, we now expect prices to increase by 3 to 4 percent over the year.

Price Growth Picks Up Speed

Real estate prices accelerated in the second quarter of 2025. Nationally, apartment prices rose by +1.2% quarter-over-quarter, while single-family homes increased by +1.0%. This marks the strongest quarterly growth since 2022 and signals a clear shift in market momentum after several quarters of below average gains.

Most large cities saw significant price growth. Zug and Lucerne recorded the sharpest quarterly increases for apartments, both rising by +2.4%, followed by Sion at +2.0%. House prices also rose strongly in Sion (+2.3%), Zug (+1.6%), and Lausanne (+1.6%). In contrast, Lugano stood out as the only city with price declines in both property types, with apartments down –1.1% and houses down –0.8%. St. Gallen also saw a drop in house prices, down -0.8%.

Over the past decade, Zug has consistently led the Swiss property market. Apartment prices there have increased by more than +70%, reflecting strong demand, limited supply, and sustained attractiveness among both domestic and international buyers. Zurich ranks second over the same period, with a ten-year gain of around +47.5%.

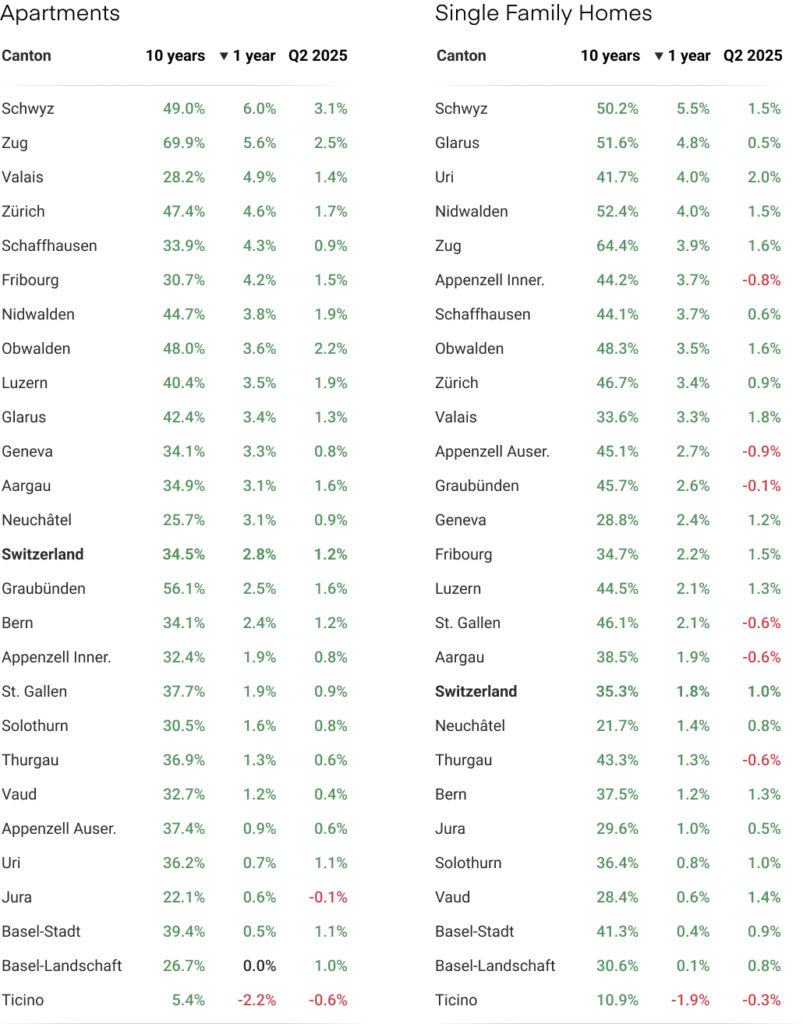

At the cantonal level, apartment prices once again outperformed houses, continuing a trend that began in 2022. Just two cantons, Ticino (-0.6%) and Jura (-0.1%), registered declines in apartment prices this quarter.

House prices fell in seven cantons, including both Appenzell Innerhoden and Appenzell Ausserrhoden, down -0.8% and -0.9% respectively. The strongest apartment gains were seen in Uri (+3.0%), Zug (+2.5%), and Obwalden (+2.2%). In the house segment, Valais led with +1.8%, followed by Zug and Obwalden (both +1.6%) and Fribourg (+1.5%).

Overall, price growth is accelerating and broadening across the country. Urban centers and central Switzerland continue to lead the market, confirming their lasting appeal. While regional differences persist, the recovery in price dynamics is now visible across most segments and geographies.

Transaction Volumes Continue to Recover

After witnessing the beginning of a recovery earlier this year, transaction volumes continued to strengthen in the second quarter of 2025. Market activity is now on track to meet or even surpass the 10-year average, marking a clear turning point after several years of subdued turnover. The rebound reflects a combination of improved financing conditions and growing buyer engagement, particularly in regions where supply remains tight and competition is intensifying.

Buyer demand has grown noticeably stronger in recent months, supported by improving market conditions and renewed confidence. The cost of financing continues to decline, with 10-year fixed mortgage rates now below 1.5% and SARON-based offers available at around 0.7%. As prices resume a steady upward trajectory, many buyers are choosing to act sooner rather than wait. The acceleration in both price and transaction trends is reinforcing a sense of urgency, especially in regions with limited supply. While Basel III regulations have introduced stricter lending requirements, these have so far been outweighed by the combined effect of lower rates, strong fundamentals, and improved buyer sentiment.

Despite the rebound in demand, supply remains critically constrained. The national vacancy rate has fallen to a historic low, and the residential construction index continues to lag behind last year’s levels. Building permits dropped by 13% year-over-year in the second quarter, adding to concerns about future housing availability. While a modest recovery in permit activity is expected in the second half of 2025 and into 2026, it is unlikely to meet the structural need for approximately 50,000 new dwellings per year. The imbalance between supply and demand remains one of the defining features of the Swiss housing market—and a key driver of continued price pressure.

Outlook: Prices Poised to Climb as Expectations Shift Toward Negative Rates

Our previous report described a stable but cautious market, with modest price growth and subdued transaction activity. In contrast, the second quarter of 2025 marks a clear shift in momentum. Prices and volumes have risen more sharply than expected, with activity now on track to meet or even surpass the 10-year average, exceeding earlier forecasts of continued below-average performance. This suggests the market is transitioning from stabilization to a more sustained recovery phase.

Since the end of the first quarter, the Swiss National Bank has lowered its key interest rate for the second time this year, bringing it to 0%. This decision was mainly driven by two factors: inflation remains very low at just 0.3%, and the Swiss franc has become even stronger, now trading at 1.25 USD per CHF, its highest level ever. Together, these trends have put pressure on the Swiss economy and left the SNB with little choice but to act. As a result, mortgage rates have dropped further, and buyers are now benefiting from some of the most favorable financing conditions in years.

Yearly transaction volume evolution, 2012 to today

One key reason the Swiss franc has reached record strength is the widening gap between Swiss and international interest rate expectations. In the United States, the recently passed “Big Beautiful Bill,” a broad economic package including major tax cuts, infrastructure investment, and expanded social benefits, is expected to significantly increase the federal deficit. This has fueled market expectations of looser monetary policy from the Federal Reserve, accelerating forecasts for rate cuts. As a result, global bond yields have declined, placing further downward pressure on long-term interest rates, including in Switzerland. With the Swiss yield curve now inverted, markets are increasingly pricing in the possibility of a return to negative interest rates by the SNB, a scenario that seemed unlikely just a few months ago.

If interest rates decline further, internal demand is likely to strengthen as affordability improves and expectations of continued monetary easing grow. For Swiss households, real estate offers a reliable hedge against inflation and long-term security, especially in a market where owning is now often cheaper than renting. However, the stronger franc raises acquisition costs for foreign buyers.

Still, Switzerland's legal certainty, political stability, and favorable tax conditions continue to outweigh currency headwinds and attract long-term international investors.

This renewed momentum creates a highly favorable environment for sellers. Well-located and competitively priced properties are now selling more quickly, as more buyers return to the market. With prices rising and competition among buyers intensifying, sellers are well-positioned to take advantage of the shift. Although global uncertainties like monetary policy and trade remain in the background, they show no signs of disrupting the current trajectory.

In the months ahead, we’ll be closely watching four key indicators: SNB policy signals, U.S. monetary moves, long-term interest rates, and Swiss housing supply. With global forces now directly shaping local dynamics, these variables will determine whether the current momentum holds or accelerates. Reflecting present conditions, we are revising our 2025 price forecast upward to +3% to +4%, with further growth expected in the coming months.

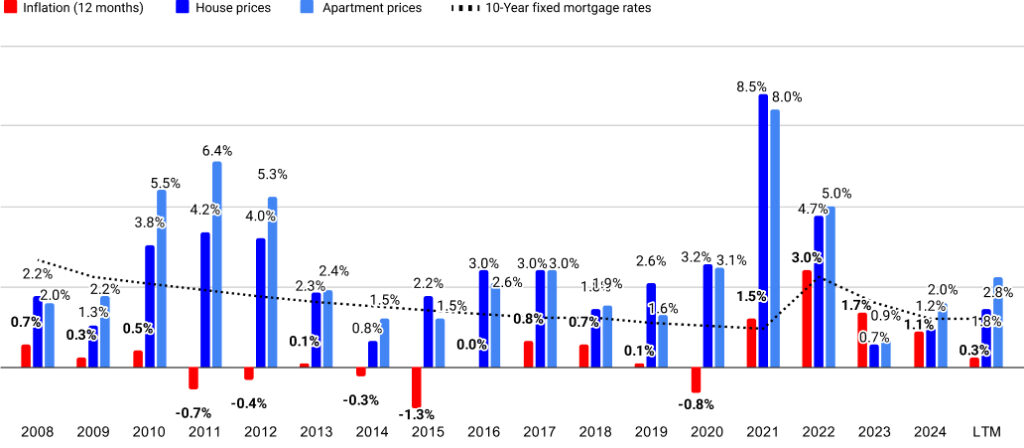

Evolution of real estate prices in relation to inflation since 2008

Agglomerations: Evolution of single family home and apartment prices

Cantons: Evolution of single family home and apartment prices

Additional information

- Property prices in Switzerland

- Online Property Valuation Online

- Download the complete version of the barometer

Press contact

- press@realadvisor.com

- +41 (0) 22 552 46 46

RealAdvisor SA

Rte de Saint-Julien 198,

CH-1228 Plan-les-Ouates

RealAdvisor AG

Heinrichstrasse 200

CH-8005 Zürich

Suisse

Suisse España

España France

France Italia

Italia Belgique / België

Belgique / België Česko

Česko Deutschland

Deutschland Nederland

Nederland Österreich

Österreich Polska

Polska Portugal

Portugal United Kingdom

United Kingdom